John DelVecchio, manager of the Active Bear ETF, received a front page mention on the Wall Street Journal for his foresight to sell short Green Mountain Coffee Roasters just before the firm announced earnings that missed Wall Street estimates.

The company lost nearly half its market cap in a single day. DelVecchio’s investors who own his Active Bear ETF (HDGE) won out.

It was just another day for DelVecchio. His fund is well-known in the actively managed fund space for being a leader in a permanently short portfolio.

Active Bear ETF’s Objective

The Active Bear ETF looks for the perfect stocks to short. We’ve covered how to short individual themes efficiently like shorting Gold and Shorting US Treasury Bonds, but for individual stock themes, DelVecchio likes to short companies that have a high probability of an earnings miss, favoring plays on reversing momentum when stocks priced for perfection report less than perfect news.

The fund orders investments by their income statements. Slumping revenue is listed as the most critical indicator of a future short sale. Share count is the least important. In between are the cost of goods sold, gross margin and SG&A costs, operating expenses, and income before tax.

In short, DelVecchio looks for indicators of future weakness hidden in a company’s income statement. If he can move the Active Bear ETF into a position before Wall Street wakes up to weakness, he can score huge gains for investors.

The Active Bear website makes a good case for permanently short portfolios. From 1983-2006, the site says, the Russell 3000 index was up nearly 900% but 39% of stocks were unprofitable investments for investors. Only 25% of stocks made up 100% of the Russell 3000’s gains. The remaining three-fourths fell in value over the 23 year period, or went into bankruptcy.

High Cost of Shorting

The Active Bear ETF is not cheap by any measure. The fund passes on annual expenses of 1.85% to investors in the form of typical management fees. However, due to the cost of borrowing shares to short, the total annual net expense ratio is listed as 3.29%.

Individual short positions make up 2-7% of the fund at any given time. The chart below shows the seven largest holdings obtained from Advisor Share’s website:

Keep in mind that the fund is actively-managed, so all positions are subject to change. The prospectus indicates that the fund is primarily interested in a business’s fundamentals when building a short position. The fund does use technical factors, however, noting that it typically does not sell short stocks that are making new 52-week highs.

The inclusion of technical analysis is a bit of a non-starter for me, but as Keynes always said, the market can stay irrational longer than you can stay solvent. Picking a declining business is undoubtedly easier than picking the top for a declining business.

Balance It Out

It is certain that the AdvisorShares Active Bear ETF will outperform long-only funds in bear markets. Due to the fund’s short history, it remains to be seen how well the Active Bear fund can perform in bull markets. With under two years of back history during one of the most broadly correlated markets of all time means that the Active Bear ETF has simply logged inverse performance to the broad market.

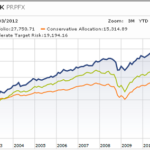

Here’s a chart of HDGE vs. the S&P500 ETF SPY:

The Active Bear ETF is negatively correlated to the S&P500 ETF (SPY) at -.89. HDGE is negatively correlated to the SPDR S&P Dividend ETF (SDY) at -.84.

Which brings me to my next point: balance this fund out with appropriate long positions. During rising markets, the Active Bear will be a drag on a portfolio. In falling markets, it will be the leading fund in your portfolio. Over the long haul, the Active Bear will need very impressive short performance to match the long-run performance of a long-only portfolio.

A Dream Fund for Income Strategies

This is an ETF that hedging dreams were made of (contrast this with the first Hedge Fund ETF launched). As a purely-short fund, it makes for an excellent fund to build your own hedging portfolio with limited correlation to the market.

Since the Active Bear’s inception, the fund shed 5.36% of its asset value. In the same period, the S&P500 Dividend ETF (SDY) rose 6.59%. Including dividends, a 50-50 portfolio would have returned 3.2% to investors in roughly 16 months.

The ability to use hedging strategies is dependent on the ability to source margin at the lowest possible rate. Using the lowest available rate on a large balance of $1 million, investors can source capital at .57% annually. Doubling up with margin on a 50-50 HDGE and SDY split gives a total return since inception of just over 6.1% in 16-months, a much better return.

The bottom line is this: the Active Bear needs alpha in excess of the fee drag to generate returns for investors. Given rigidity in the financing environment and the high management fee, it’s not yet the perfect mix for investors. Pending that the fund can attract additional capital – or competition – a reduction in the management fee could very easily provide for a low-cost hedging mechanism for generating income from dividends with little correlation to the broad market.

I find HDGE to be an interesting ETF that isn’t yet primed for individual investors. If and when HDGE lowers its management fees to more reasonable levels, this fund really opens the door to hedge fund strategy deployment by individual investors. At that point, we’ll have more performance data to evaluate a few potential hedging strategies to use with the Active Bear fund.

Disclosure: the author has no positions in any of the above securities.

{ 0 comments… add one now }